On 17th September, the German Parliament (Bundestag) passed the amendment of the Motor Vehicle Tax Act. Starting next year, the vehicle ownership tax will get an incrementally higher ecological focus. Owners of a vehicle with high CO2 emissions will be taxed more heavily, while owners of a low emission vehicle will benefit from more favorable tax breaks. The amount of the vehicle tax, paid in yearly installments by vehicle owners, depends on the size of the engine capacity and the CO2 emissions (and thus fuel consumption) of the vehicle. Under current law, owners of a vehicle pay €2.00 per 100 cm3 engine displacement in the case of a gasoline engine and €9.50 if the car has a diesel engine. If a car emits more than 95 g CO2/km, €2.00 per gram of CO2 is added.

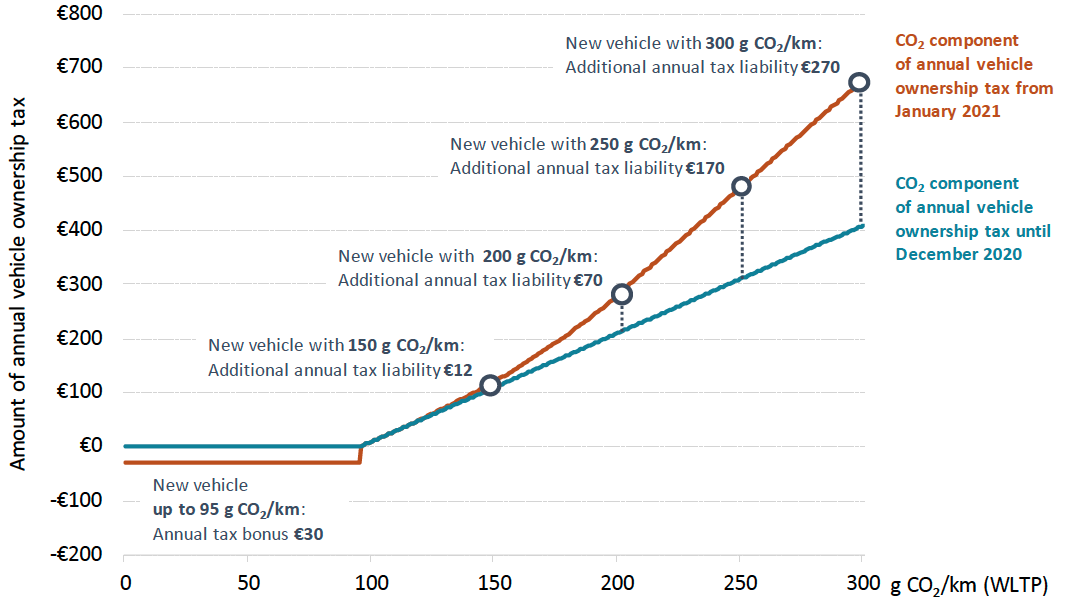

As shown in the figure above, the amended vehicle tax foresees a progressive increase of the CO2 component. Owners of a car that emits up to 95 g CO2/km (according to WLTP) will continue to incur no charges, and between 96 and 115 g CO2/km the rate remains at €2.00 per gram of C22/km. Starting at 116 g CO2/km, the rates will gradually increase up to €4.00 per gram CO2/km for vehicles with CO2 emissions above 195 g/km. For owners of a car emitting up to 95 g CO2/km there will be an annual tax bonus of €30 for a maximum period of five years if the car is registered for the first time between June 2020 and the end of 2024. The reform also includes the extension of the vehicle tax exemption for purely electric vehicles. The tax exemption, valid under the current policy for first registrations until December 2020, has been extended until December 2025 and will be granted until December 2030.

For the owner of a gasoline car that emits 150 g CO2/km, the CO2 proportion of the vehicle ownership tax increases from €110 to €122, i.e. an additional yearly tax burden of only €12. At 250 g CO2/km, the tax liability increases to €170 per year. Meanwhile, owners of a car up to 95 g CO2/km benefit from an annual tax bonus of €30.

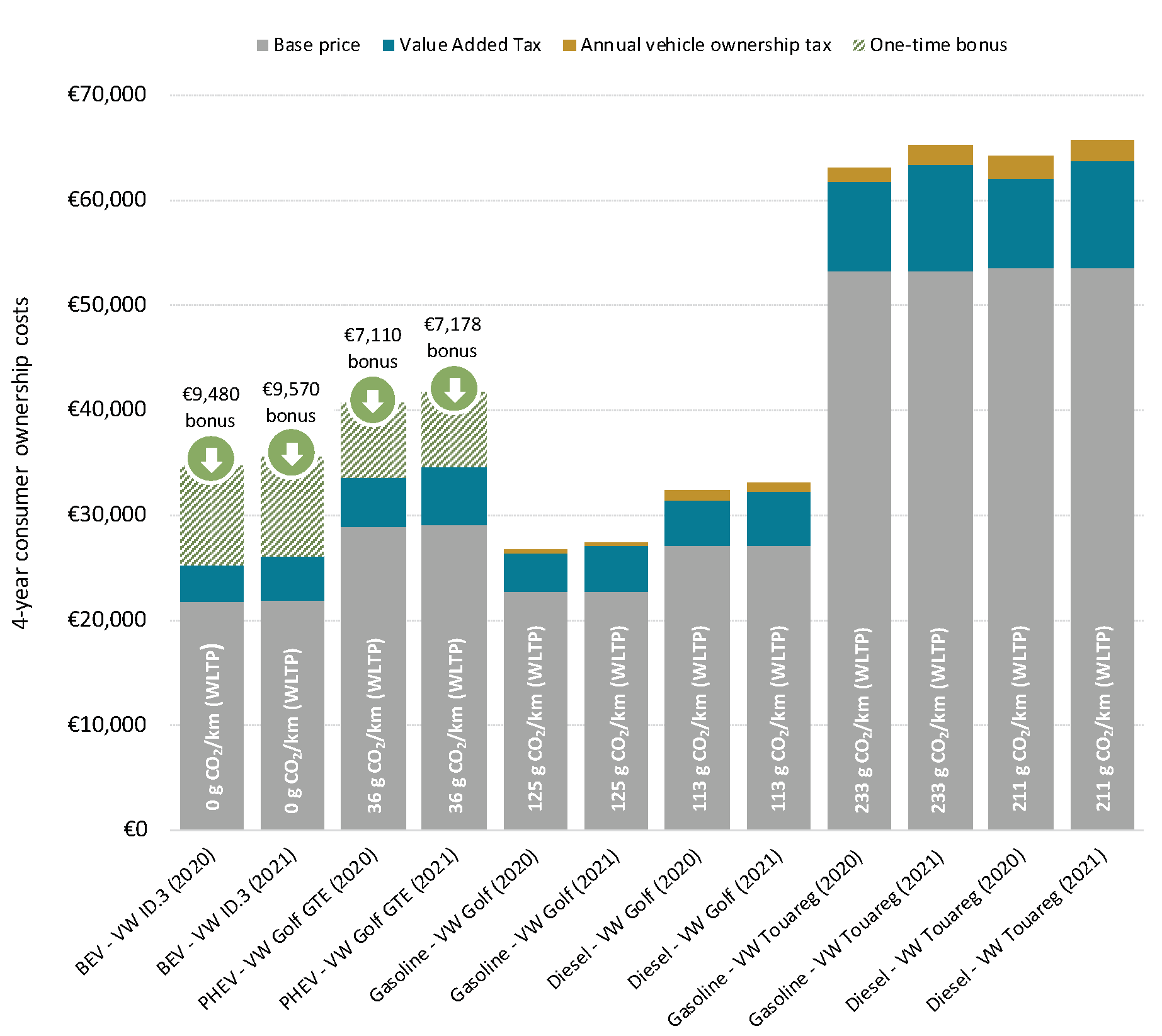

Under current policy, the vehicle ownership tax for a gasoline Volkswagen Touareg with an engine displacement of 2,995 cm3 and CO2 emissions of 233 g CO2/km (WLTP) adds up to over €1,300 over a four-year holding period. Starting next year, the owner of the same vehicle would face about €550 higher tax costs in four years as shown in the figure below. The effects of the vehicle ownership tax reform are less significant for lower emission cars. The owner of a gasoline Volkswagen Golf (1,498 cm3, 125 g CO2/km) pays €360 before and €368 after the tax reform over four years, a negligible tax disadvantage. In contrast, the purchaser of a new gasoline PHEV Volkswagen GTE pays a regular yearly tax of €28 if the vehicle is registered up to December 2020. If the purchase is delayed until the following year, the €30 tax bonus applies which means that no taxes have to be paid for a duration of five years. The owner of the BEV Volkswagen ID.3 receives a similar tax bonus for a longer duration of ten years.

When comparing current and future acquisition costs including the vehicle’s base price and Value Added Tax (VAT), as well as the vehicle ownership tax over a four-year holding period, it is clear that the vehicle ownership tax has hardly any steering effect. When further considering the costs for fuel and insurance, the vehicle ownership tax corresponds to a neglectable share of the total cost of ownership. The drop in the VAT rate from 19% to 16% in the second half of 2020 in response to the COVID-19 outbreak has an impact on the acquisition costs, but this affects all vehicle types and not only low-emission vehicles. However, the one-time bonus for electric vehicles reduces the acquisition costs significantly. In 2020 the cost reduction is €9,480 (incl. VAT for the manufacturer’s bonus share) in the case of the BEV Volkswagen ID.3 and €7,110 if purchasing a PHEV Volkswagen Golf GTE. All the cars listed in the figure above would face fewer 4-year costs if registered in the second half of 2020 compared to if they were first registered in 2021 if only accounting for acquisition costs, one-time bonus payments for electric vehicles, and vehicle ownership tax, with the latter only covering a negligible portion of the costs.

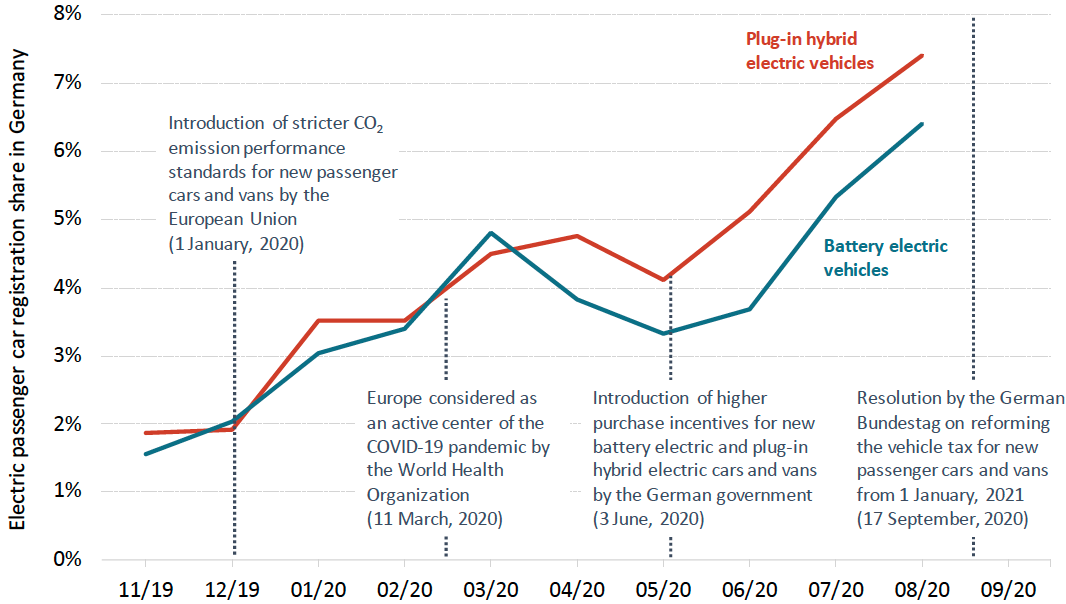

As shown in the figure below, the temporarily reduced VAT and higher purchase incentives for electric cars since mid-2020 in response to COVID-19 seem to have stabilized the market in terms of registration shares since June. Although the registration share of PHEVs dropped in May, and shares of BEVs dropped in April and May, and the share of PHEVs dropped in May, both as a result of the COVID-19 outbreak, there was a continuous increase in electric passenger car registrations shares at the beginning of the year, largely driven by the lowered European CO2 standards for new passenger cars starting January 2020.

The effect of the new vehicle ownership tax on low emission and electric vehicle purchases in favor of high emission cars has yet to be proven. In general, the direction towards a greater ecological orientation is recommendable. However, the German government could maximize its full potential by incentivizing electric vehicle purchases while at the same implementing significant tax penalties for high emitting vehicles. Such a system could also help co-finance the high purchase incentives for electric vehicles. Other countries have already implemented similar bonus-malus tax systems. In France, the purchaser of a gasoline Volkswagen Touareg with CO2 emissions of 233 g/km (WLTP) pays a national one-time malus of €20,000 and a regional tax of an average €950 upon registration plus an annual vehicle ownership tax of €160. In Sweden, the malus on vehicle ownership tax for the same car would be more than €1,300 annually over a duration of three years and a lower annual rate of almost €300 in subsequent years. In comparison, the yearly rate in Germany based on the reformed vehicle ownership tax will only be just over €450 from the first year on. To reach the country’s climate goals, a more progressive approach would be to set an even stronger political signal towards low-emission vehicles. The upcoming months will show if the reform of the vehicle tax can contribute to accelerating the end of the combustion engine car.

Please click here to view the full press release.

SOURCE: ICCT