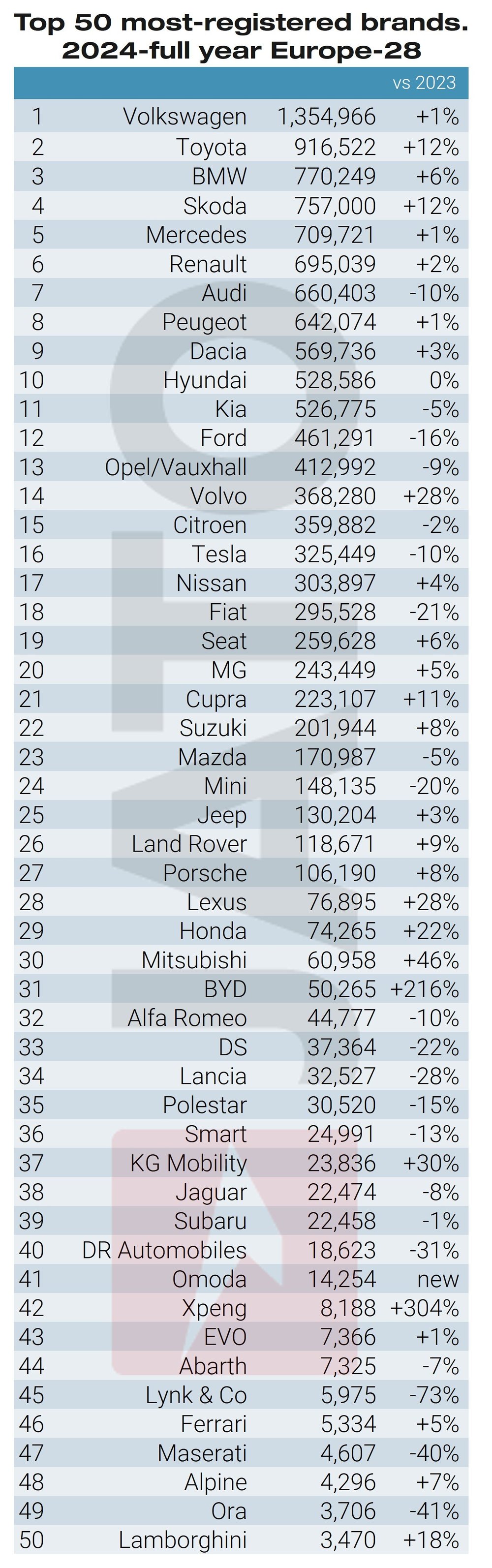

Europe’s new passenger car market grew by 0.9% last year. This is according to new data from JATO Dynamics, which found that 12,909,741 new passenger cars were registered across Europe-28 in 2024.[1]

Despite the slight uptick in registrations, 2024 was the fifth year of muted registrations figures when compared to pre-pandemic levels. Europe’s car market has shrunk by almost 2.9 million units since the arrival of the pandemic in 2020.

“Overall, when you consider the range of challenges facing Europe’s automotive industry, the results for 2024 are not overly negative,” commented Felipe Munoz, Global Analyst at JATO Dynamics. “However, you would expect any other industry to have shown significant signs of recovery by now, and there is very little evidence that the automotive industry will return to the pre-pandemic reality. The higher cost of vehicles, the rise of working from home, inflationary pressure on wages and the emergence of new transportation solutions are among the reasons why Europeans have stopped buying brand new cars,” Munoz continued.

Fewer electric cars, more hybrids

2024 was not a positive year for sales of electric vehicles (EVs) in Europe, with the slowdown in growth that the industry began to see signs of in 2022 resulting in a drop in sales last year. Sales grew +107% year on year between 2019 and 2020, +63% between 2020 and 2021, +29% between 2021 and 2022, and +28% between 2022 and 2023. However, 1,985,996 units of new passenger EVs were registered in EU28 in 2024, marking a year-on-year decline of 1.2%.

The drop in registrations was also reflected in the market share of BEVs in Europe, which decreased slightly from 15.7% in 2023 to 15.4% last year. A lack of clarity about incentives for BEVs, the high average retail price of new models and low residual values – as well as concerns about charging infrastructure across the continent – are among the reasons behind the decline. Despite the drop recorded last year, the situation is expected to improve over 2025 as the average price of a BEV continues to fall in Europe, largely due to the introduction of less expensive models from mainstream automakers.

Norway maintained its poll position in 2024, with BEVs holding the largest market share (88%). It was followed by Denmark (51%), Sweden (35%) and the Netherlands (34.7%). Denmark, Belgium, Norway, Luxembourg and the Netherlands were the five countries in Europe where BEVs gained the most market share year on year, while the opposite occurred in Germany, Ireland, Finland, Romania and Sweden.

From a manufacturer perspective, the BEV market did not change significantly in 2024. The Volkswagen Group remained the top-seller, with more than 427,000 units of its electric models registered in 2024. Its share of the BEV market fell slightly from 22.2% in 2023 to 21.5% last year and remains below its share of the wider new passenger vehicle market, which stood at 26.1% in 2024. Tesla followed in second position, despite increased competition from other players and its Model 3 being unable to offset significant losses while consumers waited for the arrival of the new Model Y. In third place came Stellantis, which remained in the top three producers of BEVs despite posting a 10% drop in volumes. Elsewhere, BEVs made up a greater part of the sales mix for BMW Group and Geely last year.

Hybrid vehicles: a halfway house?

Although not all carmakers offer fully hybrid models, the segment recorded year-on-year growth of 21% between 2023 and 2024, and all carmakers that offered fully hybrid vehicles posted growth last year.

Out of a total market of 1,529,806 units registered in 2024, Toyota accounted for 738,500 units. Almost one in two hybrid vehicles registered in Europe in 2024 had a Toyota or Lexus logo, and 75% of registrations of Toyota passenger cars were hybrid vehicles.

Renault Group followed with almost 300,000 units, up 49% year on year, while Hyundai-Kia, Nissan and Honda accounted for the rest of the top five. Volkswagen Group, Stellantis, BMW Group, Mercedes-Benz and Geely were a few of the manufacturers absent from this segment.

Hybrids have become increasingly popular due to the comparatively high average retail price of BEVs and concerns about charging infrastructure. According to a recent JATO study, the average retail price of a hybrid available in the Eurozone in 2024 was €42,222, compared to €62,709 for a BEV.

China continues to grow in influence

According to JATO estimates, almost 21% of total new passenger vehicles registered in EU28 in 2024 came from plants in Germany.[1] However, Germany lost market share in this respect to Czechia, the third largest country of origin for vehicles in Europe, behind Spain. France came in fourth position, despite volumes from French factories falling by 3%, while Romania rounded off the top five.

The most significant trend was China becoming the sixth-largest country of origin for new vehicles registered in Europe. Between 2023 and 2024, it outsold the United Kingdom, Turkey, Japan and South Korea. “Last year, more of the cars registered in Europe came from China than Japan,” Munoz commented. “China’s influence in Europe – both from Chinese OEMs and Chinese-made vehicles – is growing steadily. Their products are highly competitive, but it remains to be seen just how much the introduction of tariffs will impact its growth,” Munoz continued.

SAIC Motor, Geely, BYD, Chery, and BMW Group were the top best-selling companies of Chinese assembly origin cars in Europe last year.[1]

Record market share for SUVs

SUVs remained the best-selling vehicle segment in Europe, despite growth of the category moderating over the past three years. 54% of total registrations in Europe in 2024 were SUVs – a record market share for the segment. In total, consumers in Europe bought 6.92 million SUVs, up 4% from 2023.

Compact SUVs (C-SUVs) were the most popular type within the category, accounting for 42% of total SUV registrations last year, followed by smaller models (B-SUVs), with 36% market share. However, the largest growth came from luxury SUVs, registrations of which were up 13% to 56,300 units.

Almost one quarter of the total number of new SUVs registered in Europe last year were from Volkswagen Group, with the T-Roc and Tiguan among the top ten best-selling models in the category. Stellantis was the second best-seller with almost 800,000 units – down 7% from 2023 – while Hyundai-Kia came in third place with 705,500 units, down 1%.

SUVs were a key segment last year for other automakers including Jaguar Land Rover, Geely, Honda and SAIC Motor, while the segment made up less than half of total sales for Stellantis, Renault Group, BMW Group, Mercedes-Benz and Mitsubishi.

The Dacia Sandero leads for the first time

The end of the Volkswagen Golf’s reign as Europe’s most popular model of passenger vehicle in 2021, was followed by yearly changes in the first position. In 2022, the Peugeot 208 gained the crown; in 2023 it was the Tesla Model Y; and the Dacia Sandero – which has been in the top three best-selling models since 2021 – took first place last year.

The popularity of the Sandero is largely down to its status as one of the most affordable car models available in Europe. Its price allowed it to top the model ranking in two markets – Spain and Portugal – while it was among the top five best-selling models in France, Italy, Belgium, Austria and Romania.

In 2024, registrations of the Tesla Model Y fell by 17% – the steepest drop among the top 36 models – as it dropped to fourth place in the model ranking and lost its crown as Europe’s best-selling vehicle in the process. The downturn can be partly attributed to the decreasing impact of price cuts offered by Tesla last year in comparison with 2023 – a factor that helped propel it to top spot – and increasing competition within the market. Despite the downturn, the Model Y was the best-selling car in the Netherlands, Sweden, Switzerland, Denmark and Norway last year.

Elsewhere, the Volkswagen Golf regained some traction due to better-than-expected results in markets including Germany, Italy, Austria, and Spain. Nevertheless, the 215,700 units registered last year pale in the comparison to the 445,600 and 410,300 units registered in 2018 and 2019 respectively. The Golf and the Tiguan posted the highest increase in volume among the top 20 models.

Further down the model ranking, strong results were posted by the BMW X1 (+30%), Seat Ibiza (+34%), Opel/Vauxhall Astra (+38%), Jeep Avenger (+93%), Suzuki Swift (+38%), Mercedes E-Class (+33%), Seat Leon (+39%), Mercedes EQB (+58%), Mercedes GLC Coupe (+37%), and the BMW X2 (+54%).

Among the new cars that were introduced between late 2023 and 2024, 78,000 units of the Volvo EX30 were registered, as it became Europe’s third best-selling BEV. Volkswagen registered 32,200 units of the ID.7, hitting the top 20 BEVs; the new MG3 posted decent sales figures of 31,300 units; 26,300 units of the Fiat 600 were registered, below the 37,400 units of the 500X registered in 2023; 24,100 units of the new Renault Scenic E-Tech were registered; while 21,400 units of the Lexus LBX were registered – far ahead of its rival the Alfa Romeo Junior, for which only 5,300 units were registered.

SOURCE: Jato